Долгосрочный технический анализ

Before drawing up the chartist's trading plan the dealer studies historical data for forecasting and selects a traditional or modem chart for study or a combination of both.

He must choose chart patterns of note to identify a potential continuation/reversal or neutral trend with trigger level and extension target, pay special attention to moving averages and oscillators signals for an indication and confirmation of the trend, and anticipate its turns.

For in-depth analysis dealers usually use the Elliott wave count.

Generally most forex dealings are based on the dollar. And it is the movement of the dollar which is moving the financial market. The basic idea of making a profit is to buy dollars low and sell high.

The dealer can never be certain of what may occur. Unfortunately forecasting is not a science but an art and anything can happen.

By January 1994 hardly anybody thought that the dollar could fail to cross 1.80 to the Deutsch Mark. The greenback did and made forecasters shy for 1995. In fact most studies see the dollar rising but, burned by experience in 1994, predict only modest rates. Right now (02/95), as levels of about 1.50 can be seen, predictions range from 1.65 to 1.75 for the end of 1995.

Long Term Technical Analysis

Dollar/DM Forex Rate Moves in 1995.

In December. 1994 the greenback started an upward correction which was followed by a retracement in March. Mid of May 1995 the dollar remained in the 1.36 / 1.39 consolidation range. In August the US dollar drifted around between 1.35 and 1.42 of the German Mark. By the end of the year dollar/DM broke above 1.44. The continual downward trend since the start of 1994 seemed to be finally over. All the moves of the USD/ GEM are plotted on the Chart (Jan. 1996) and analysed in the articles below.

Dollar consolidates (Dec. 94)

Vocabulary

hike — повышение

At the FOMC meeting of the FED on the 14th of November. the long expected interest rate hike became reality. The FED increased both the discount and the fund rates by 0.75 each to 4.75% and 5.5% respectively. Even before the summit, the

FED(FRS) — Федеральная резервная

greenback started an upward correction, which was continued

Federal Reserve система США (ФРС)

by the interest rate hikes, which were slightly above expectations. The international interest rate scenario has changed dra

System

matically over the last months. Contrary to the situation at the beginning of the year, where the dollar rates were around 2% below the DM rates, now the dollar rates for all maturities show a premium above the DM yields of 0.5% to 1%, this factor has to influence forex trade as well.

As the bearish sentiment will not be forgotten for a while, we expect a Range trading between 1.53DMand 1.75DM till the end of the year. but at least the lows should be behind us.

Improving charts

After an extend test of the lows at 1.50 DM, the market returned into the consolidation pattern between 1.53 and 1.58, which developed in the summer.

FOMC — Комитет по операциям на

Federal открытом рынке (ФРС) США

Open Market

Commettee

ju: maturity — ценные бумаги со сроком погашения

range trading — торговля в канале (коридоре)

Dollar breaks 1. 42 DM on the upside Dollar crisis seems to be over June, 95)

Mid of May the dollar broke the heavy resistance around 1.42 DM and left the 1.36—1.39 consolidation range on the upside. As this break-out was followed by several tests on the downside, at least from the technical viewpoint the cyclical lows should be behind us. Another bullish item is that this scenario occured without any intervention by any central bank. Obviously the market found a balance and finally heavy fund buying pushed the greenback higher. Fundamentally this action was backed by the announcement of stringent American trade sanctions against Japan. How important these punitive measures have already proved to be was shown by the last trade balance report. The US — Japanese trade deficit widened bv30%. despite the recent Yen surge and a lot of rancour between Mikey Kantor and his Japanese counterpart. Having tested the 80 Yen support twice, the dollar bounced back by 10% within two weeks.

The dollar finds a floor (Aug. 95)

The US dollar has been drifting around between 1.35 and 1.42 to the German mark for several months now, but at least the continual downward trend since the start of 1994 seems to be fmalv over. At the start of May a breakout to 1.45 was quickly brought to a halt. Many analysts believe though, that the dollar is between 10—20% undervalued, even if the recent data emerging from the US economy has altered that relationship slightly. The most recent interest rate cut by the FED was clearly seen as being their response to the negative economic data. It was the first cut in one and a half year, a period which has seen seven rises. Many experts predict that it will not be the last.

Buba lowers rates, but not to spur growth German interest rate cut (Jan. 96)

The Bundesbank (Buba) in Frakfurt cut the discount and Lombard rates by half a percent last month, taking them to 3 and 5% respectively. The long-awaited, but little hoped for, announcement took the markets bv surprise, following a series of rather mixed signals corning out of the Buba. Hans Tietmever. president of the bank, denied that there had been any ambiguity about the bank's intentions when he made the decision public. This brings German interest rates to their lowest level since mid-1988. and is the third such reduction within a year. It appears that the Buba was persuaded to make the decision after reviewing the progress of M3. the broad

агрегат МЗ плюс банковские депозиты частного сектора в инвалюте (Великобритания)

to run out — выдохнуться of steam 62

funds — деньги, ссужаемые банкам федеральным резервным фондом

i stringent — строгий ^

Ju: punitive — карательный

ае rancour — вражда

э: to emerge — появляться

е respectively — соответственно

to take by — удивить surprise

эе ju ambiguity — двусмысленность

to make public - обнародовать

money supply figure, which showes a sharp reduction over the previous year. M3 did put on speed in the middle of the year, but then ran put of steam, and it was this slowdown which prompted the Buba to make its move. Predicted M3 growth targets of 4 — 6% were not met. mainlv due to a slowdown in economic activity. The Buba statement maintained that the latest interest rate policy was intended to put money supply and the economy on a similar oath. Other contributory factors were low inflation

ju: 'due to

to drift into recession

a: to enhance

л to under pin

— из-за

- скатываться к снижению деловой активности

- стимулировать подпирать

and low potential for steep price rises and the continuing strength of the mark, whose protection is one of the Buba's main aims. The bank also painted a more optimistic picture of German economic potential than has been fashionable recently. and the president pointedly stated that he sees no grounds for the fear that Germany is drifting into recession. This rate cut served to underline his, and the bank's, view that economic frowth would be enhanced, not underpinned, by the cut. Analysts soeculate that a weakening of the economy or a collapse of the French currency, could force the Buba to act again and lower rates.

Comprehension Questions

1. What does the dealer have to study and select for forecasting?

2. What are chart patterns for?

3. Why did the greenback make forecasters shy for 1995?

4. What were the predictions for the end of 1995?

5. Was the continual downward trend over in 1995?

6. What brought dollar yields well above DM rates in December 1994?

7. When did the dollar break 1.42 DM on the upside?

8. How much did the US-Japanese trade deficit widen in June 1995? i 9. Did the dollar find the floor in August 1995?

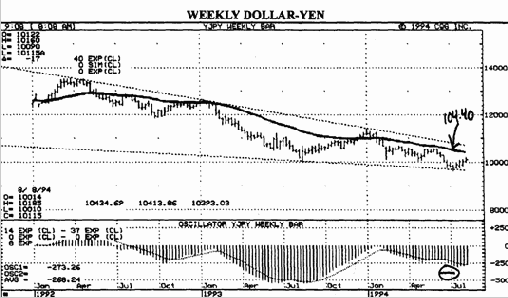

called a corrective situation within a bear market if price is rising toward a still falling trend indicator. The weekly oscillator is also rising from a bearish level.

The short-term picture for dollar-yen should stay mildly

favorable for the USD as long as values hold over a support zone set by a rising 40-day moving average at 100.30 and the rising trendline off the July lost at 98.80—98.70. Dips should be supported until that area is broken. Near-term upside targets are 102.10—20 and 103.20. These values represent 62 to 75% retracements to the June/July downleg in the dollar. If a larger bear phase is still in progress, those are exceptable retracement

parameters for bear market corrections. Closing action under 98.70 should indicate the start of a new, and probably final, downleg for the dollar against the yen. The target for a new downleg will be 95.50-94.50. Secondary technical aspects are somewhat mixed. Market sentiment indicators are neutral.

There are no important cycles working for price right now. The seasonal tendancy for the yen versus the dollar is to rally from August into October. If new topping signs show in the dollar as the seasonals, one more low later this fall is possible.

ou

close

— курс (цена) при закрытии торгов

ou

low

— низкое значение(цены)

ai

high

— высокое значение(цены)

э

bottom

— самый низкий уровень

fisher

— ловец

e

correction

— движение цены в направлении, обратном тренду(коррекция)

ai

to 'highlight

— высвечивать

Compresension Questions

1. How much has the yen appreciated against the US dollar for 4'/^ years?

2. Why is this appreciation coming to an end?

3. What was the result of the yen rise?

4. What was the trade surplus?

5. What do rumours say about Japanese interest rates?

6. Is unemployment in Japan high or low?

Exercises

Ex. 1. Put question to the underlined words.

Ex. 2. Read and translate the text.

Ex. 3. Using the chart and the various technical studies and trendlines describe USD/DEM price movements from

May 93 to Jan 94 and USD/JPY from 85 to 93. Ex. 4. Translate the dialogue from English into Russian in writing and from Russian into English orally.

Dialogue

Client: What is your medium term outlook for dollar/DM in 1996?

Broker: Dollar/DM broke above 1.4435 in December 95 But the impetus was weak.

CL: Resistance at 1.4580 was too dense for it. Wasn't it?

Br: Yes, you are right. But the subsequent retracement from this area has allowed the market to build strength for

another assault on the upside. Cl: What could be a possible target area of the assault?

Br: A break above the 1.4545/80 zone is likely over the coming month, it may trigger a rally to 1.5045 initially. Cl.: Thus the medium term objective remains 1.56/1.58. Br.: That's right. Dips should continue to find good support in the 1.4280/65 band. Cl.: What can you recommend?

Br: I would advise you to hold longs, adding on dips to 1.4340/00, keeping the stop/reverse below 1.4265/60. CL: Shall I cover longs?

Br.: Cover longs on rallies to 1.4545/80, reinstating on a break. Cl.: Is there any danger of a correction? Br.: Loss of 1.4265 will signal a deeper correction towards the 1.40/1.38 area. My advice is: reinstate longs here, stop/reverse below 1.37.

Has the starting rise in the Yen finally run its course?

Doubts rise over yen hausse in Feb. 96

In the space of 4 1/2 years the Yen has appreciated more than 60% against the US dollar. It is starting to look like this is coming to an end. This is mainly because the Japanese economy is having trouble keeping up with the international economic upswing and maintaining its competitiveness with the strong Yen.

Exports suffer

The rise in the Yen has dealt a blow to Japan's export orientated economy. Partial relief to exporters has come from rationalisation and moving production to cheaper countries. Even the famous trade surplus has shown signs that the tide is turning. Although the surplus reached 121 bn USD, this was just 0.8% higher than 1993. Motor vehicle production, the vanguard

of Japan's economic might, decreased by 6%. to 10.55 mio vehicles. Car production suffered most, falling by 8%.

Monetary policy

Rumours also surfaced that Japanese interest rates will fall. At 1.75% for the Discount rate and 3% for the Prime rate, they are by far the lowest in any of the industrialised nations. Altogether more positive is the consumer price inflation, which rose by 0.2%. and the producers index which dropped by 1.3% Unemolovment. at 2.9%. is low in comoarison to other countries, even if the figures tend to be massaged.

Dollar -Yen: Recovery or Correction Gul. 94)

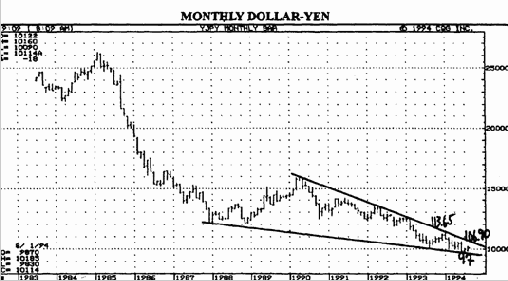

The USD recovery is impressive on a short term basis. A major trendline support level at 97.00 last month is forging ahead through many levels of resistance. The dollar buyers were attracted by the rally effort through an old trendline off the 1993/94 lows at 100.40—100.50. The long term technical analysis still views USA strength as corrective to the long bear market. A large coiling down trend pattern since 1988 is still evident on the monthly chart. The dollar tested and bounced off the low end of the formation at 97.00. The upper boundary at 106.50—106.90 should be watched. A monthly close over here points to the end to the bear market and the start of a major USD base. An uptrend cannot be expected until the early 1994 high at 113.65 is removed. The weekly chart also reveals the large coiling pattern. Near the 103.90—104.40 area a falling 40 week moving average trend indicator can be seen. The market condition could be

Vocabulary

to deal a blow — нанести удар tide is turning — положение меняется bn (billion) — миллиард mio (million) — миллион

S3:

to surface — возникать by far — значительно

ju: consumer price — потребительская цена

ju: producers index — индекс промышленных цен

о: to massage — массировать, обрабатывать

л

upside — повышательное движение цены

о: target — плановая, ожидаемая цена

е exceptable — составляющий исключение

test — приближение цены к точке сопротивления (поддержки

01

coil — спираль

au to bounce off — отскакивать

au boundary — граница

ou slope — наклон,скат

ai sideways — цикл с горизонтальным движением цен

л

recovery — подъем рыночной конъюнктуры

о: to forge — медленно двигаться вперед

ае rally — повышение

64

Содержание